Docket No. RM26-6-000

In today’s order,[1] the Commission establishes the five-year oil pipeline index as (PPI-FG) – 0.55%. I dissent from that result because I disagree with the order’s decision to (1) apply a uniform return on equity (ROE) modification to account for changes in the Commission’s ROE policy, and (2) adopt a data set trimmed to the middle 80% of cost changes rather than the middle 50%. Instead, I would establish the five-year index value as (PPI-FG) – 1.68%, which is consistent with relevant precedent and supported by the record.

I. Background

The Commission’s oil pipeline indexing methodology is a ratemaking construct unique to its regulation of transportation rates under the Interstate Commerce Act (ICA). Developed in response to Congress’ directive in the Energy Policy Act of 1992 to establish a “simplified and generally applicable” ratemaking methodology,[2] the index allows pipelines to annually adjust their rates subject to a cap rather than relying on lengthy, complex cost-of-service proceedings.[3] While the index is the predominant method used to set rates under the ICA, pipelines have multiple options for establishing and updating their rates, including cost-of-service filings, qualifying for market-based rates, and the use of negotiated or settlement rates, particularly for the development of new infrastructure.[4]

In 1993, Order No. 561 set the “Kahn Methodology” as the approach that the Commission uses to collect and trim cost data provided by the pipelines[5] and to compare their cost changes against an inflation rate in the economy, as measured by the Producer Price Index – Finished Goods (PPI-FG) set by the Bureau of Labor Statistics. The Commission updates the resulting oil pipeline index every five years through a review of industry-wide cost changes over the preceding five-year period. The Final Rule succinctly summarizes how the calculation works:

Each pipeline’s cost change is calculated on a per-barrel-mile basis over the previous five-year period (e.g., the years 2019-2024 in this proceeding). To remove statistical outliers and potentially spurious data, the resulting data set is trimmed (e.g., to the middle 80% or middle 50%) by removing an equal number of pipelines from the top or bottom of the distribution. The Kahn Methodology then calculates three measures of the trimmed dataset’s central tendency: median, mean, and weighted mean.[] The Kahn Methodology calculates (a) a composite central tendency by averaging the median, mean, and weighted mean and (b) the difference between the composite central tendency of per-barrel-mile cost changes and the percentage change in PPI-FG over the prior five-year period.[]

This measurement, the difference between observed pipeline cost changes and PPI-FG, generates an index that the Commission applies for the prospective five-year period, that is PPI-FG plus or minus a percentage.[6] This means that if PPI-FG were 3% in a particular future year, the pipelines’ rates are allowed to increase by 3% plus or minus the amount set by the 5-year oil pipeline index.[7] Each year, effective July 1, pipelines are allowed to adjust their ceiling rate using that index,[8] which sets the maximum rate that a pipeline can charge for transportation services if it is using the indexing methodology.

This proceeding addresses the index for the upcoming five-year period (July 1, 2026 – June 30, 2031), relying on data submitted by jurisdictional pipelines for the 2019-2024 period. Among the issues raised in the record are: (1) whether the Commission should adopt changes to pipelines’ filed 2019 ROEs to account for a change in the Commission’s oil pipeline ROE policy; and (2) a standing question in each five-year cycle, of what data trimming the Commission should apply.[9]

II. The Order Errs by Adopting a Uniform ROE Modification to Diverse Pipelines’ Reported 2019 ROEs

As discussed below, I disagree with the order’s adoption of a proposal by the Liquid Energy Pipeline Association (LEPA) to apply a uniform ROE modification to the wide ranging and diverse pipelines’ 2019 reported cost data. LEPA’s proposal is conceptually flawed, conflicts with relevant Commission precedent, and is inconsistent with the pipelines’ independent derivation of their own reported ROEs. As a result, LEPA’s proposal does not yield a credible ROE value to be included in the 2026-2031 oil pipeline index.

A. Background

Beginning with the 2015 index cycle, the Commission has used data from page 700 of Form No. 6 as the basis for its index calculation. Whereas the Commission’s prior calculations relied on alternative proxies for each pipeline’s cost of capital (including ROE),[10] the data includes a calculated cost-of-service for each oil pipeline based on inputs including expenses, depreciation, and return based on the rate base of investments net of depreciation and the rate of return, which itself includes each pipeline’s reported ROE. This cost-of-service rate is then divided by the pipeline’s total barrel-miles to determine the cost per barrel-mile. The Commission then compares that cost per barrel-mile of the two end points of the study period (here 2019 and 2024) to calculate the cost growth rates for each pipeline. After trimming the data set, the Commission calculates the average of the mean, weighted mean, and median growth rates in cost per barrel-mile of all applicable pipelines minus the then relevant PPI-FG to determine the index level to be applied to the next five years. These steps were specified in the Kahn Methodology.

In 2019, the Commission revised its ROE policy for electric utilities to, among other revisions, combine use of its existing Discounted Cash Flow (DCF) methodology with the Capital Asset Pricing Model (CAPM) methodology.[11] In 2020, it extended that methodology to oil pipeline and natural gas rates, which previously relied only on the DCF methodology.[12] As a result, following issuance of the ROE Policy Statement, each oil pipeline is required to annually derive and report its ROE on page 700 using the average of ROEs calculated using the DCF and CAPM methodologies (ROE Policy Change).

In the ROE Policy Statement, the Commission recognized that the ROE Policy Change could have implications for the upcoming 2020 index cycle, which was based on filed page 700 data from 2014-2019.[13] The Commission expressly “encourage[d] oil pipelines to file updated FERC Form No. 6, page 700 data for 2019 reflecting the revised ROE methodology established herein,” and noted that “[a]lthough the Commission will address this issue further in the five-year review, reflecting the revised methodology in page 700 data for 2019 may help the Commission better estimate industry-wide cost changes for purposes of the five-year review.”[14] The Commission subsequently issued a notice, establishing July 21, 2020 as the deadline for pipelines to voluntarily submit updated 2019 data reflecting the ROE Policy Change and clarify how they derived their filed 2019 ROEs.[15] Only two pipelines submitted updated 2019 data in response to this invitation, and as a result, the vast majority of pipelines did not revise their 2019 data to incorporate the ROE Policy Change. However, pipelines presumably began calculating and reporting their ROEs prospectively to reflect the ROE Policy Change (i.e., reporting ROEs that averaged values derived using both the DCF and CAPM methodologies, including for the year 2024, the end point of the period under consideration in this index cycle).

The current five-year index cycle relies on the pipelines’ cost data from 2019-2024. In the NOPR,[16] the Commission proposed to calculate the index level with the pipelines’ reported 2019 data, without having the Commission adjust the 2019 data to reflect the ROE Policy Change. The NOPR recognized that the “Commission has never adjusted ROE in a prior index proceeding,” and stated its “concern[] that adjusting the data in light of the ROE Policy Change would be a complex and difficult endeavor that would be inconsistent with index’s purpose as a simplified and streamlined process.”[17]

In response, LEPA submitted a proposal specifically designed to account for the ROE Policy Change, i.e., that each oil pipeline’s ROE will be determined by averaging ROEs derived using the CAPM and DCF methodologies. LEPA proposes a modification to each pipeline’s FERC Form No. 6, page 700, filed ROE for 2019 for purposes of calculating the index. Specifically, instead of using each applicable pipeline’s 2019 filed ROE, LEPA proposes to average each pipeline’s originally-filed ROE, which varies by pipeline, with a single CAPM-derived ROE of 8.3% (ROE Modification). This value resulted from the methodology and proxy group from a litigated proceeding involving a single pipeline, Colonial, with adjustments for different financial conditions for the test year of that proceeding and the 2019 Form No. 6 data.[18] The effect of the ROE Modification would be to blend a uniform, industry-wide ROE value with each pipeline’s reported ROE for 2019, and to then use that blended value and compare it to the pipeline reported data for 2024, to set the index.

B. Commission Precedent and the Record Do Not Support Adoption of a Uniform ROE Modification to Address the ROE Policy Change.

My assessment of the record on the ROE Modification is guided by the following analysis: (1) is it appropriate to adjust the originally-filed 2019 data to account for the ROE Policy Change; (2) if yes, does the record establish that there is a methodologically-sound and generally-applicable modification that is consistent with the simplified design of the Commission’s indexing methodology; and (3) if yes, does the record establish what that generally-applicable modification should be. The Commission should only adopt a proposal if that modification satisfies all three questions. LEPA’s proposal does not. Instead, the order’s tinkering with the index methodology through the ex post application of the ROE Modification introduces methodological infirmities, is inconsistent with Commission precedent, and is unsupported by the record. Accordingly, I would use the pipelines’ filed 2019 data to determine the index, rather than making a modification to account for the ROE Policy Change.[19]

1. The Use of a Uniform ROE for Oil Pipelines Is Conceptually Flawed

As a threshold matter, the ROE Modification rests on a simple but incorrect premise: that a single ROE can be derived for an industry as diverse as the oil pipeline sector. This premise conflicts with the basic design of the Commission’s ROE policy.

An oil pipeline’s risk profile is central to the Commission’s ROE analysis. As the Commission explained in the ROE Policy Statement:

Because most…oil pipelines are wholly owned subsidiaries and their common stocks are not publicly traded, the Commission must use a proxy group of publicly traded firms with corresponding risks to set a range of reasonable returns. The firms in the proxy group must be comparable to the pipeline whose ROE is being determined, or, in other words, the proxy group must be “risk-appropriate.” The range of the proxy group’s returns produces the zone of reasonableness in which the pipeline’s ROE may be set based on specific risks. Absent unusual circumstances showing that the pipeline faces anomalously high or low risks, the Commission sets the pipeline’s cost-of-service nominal ROE at the median of the zone of reasonableness.[20]

These statements emphasize certain critical elements of the ROE analysis: (1) these assessments are pipeline-specific; (2) the proxy group and corresponding zone of reasonableness for each pipeline must be composed of publicly traded firms with comparable risk profiles to the pipeline; and (3) the specific pipeline’s relative risk profile within that zone of reasonableness will determine the placement of the pipeline’s ROE in that zone. And these requirements make sense, as a pipeline’s rate of return should be tailored to the level needed to secure capital investment. That level will naturally and properly vary based on a pipeline’s specific characteristics and risks, which could include, among others: (1) the level of competition that it faces; (2) whether its revenues vary significantly or are relatively stable; (3) the age, condition, and location of its system; (4) the types of products it transports; and (5) physical or cyber risks to its system.

LEPA’s proposal turns this analysis on its head. Instead of tailoring an ROE analysis to pipelines’ specific risk profiles, LEPA compresses the entire industry into a single, uniform proxy group and risk profile, then assigns the entire industry a single CAPM-based ROE. A simple example highlights the defects in this approach. Take two companies that are part of the data set: (1) South Bow, which operates a major interstate pipeline system that runs from Canada to the Gulf and reports earnings in excess of $1.3 to $1.4 billion in revenues; and (2) Andeavor Gathering, which operates a small gathering system and reports annual revenues between $3.5 and $5.6 million. These pipeline companies face very different risks: they operate in geographically different markets, have drastically divergent level of revenues, and operate in different sectors of the industry (long-distance transportation versus localized gathering). Yet, under LEPA’s proposal, these pipelines are deemed to face comparable risk and are assigned an identical CAPM-based ROE value.

LEPA’s proposed approach is at odds with the Commission’s ROE policy. And as discussed in the next section, the Commission recognized the inherent contradictions and complications created by imputing a single ROE to the entire industry when it rejected a similar proposal from shippers in the last index cycle.

2. The Commission Has Considered and Rejected Application of a Uniform, Industry-wide ROE for Oil Pipelines

As the NOPR and Final Rule acknowledge,[21] this is not the first time the Commission has considered a proposal to adopt a uniform ROE for purposes of the five-year index. For reasons that apply with equal force to this proceeding, the Commission rejected that previous proposal as inconsistent with its ROE precedent and the simplified and streamlined design of the oil pipeline indexing methodology.

In the most recent 2020 cycle, Liquid Shippers proposed to replace the pipelines’ self-reported ROEs (which presumably reflected the pipelines’ own assessment of their relative risk profiles) with a single, industry-wide ROE values for both 2014 and 2019.[22] Echoing arguments raised in this proceeding, Liquid Shippers claimed that “if all oil pipeline rates were litigated at the same time, absent unusual circumstances, the Commission would adopt the same ROE for every pipeline because regulated pipelines typically fall within a broad range of average risk,” and that the pipelines’ “reported ROEs conflict with this principle because they vary substantially.”[23] Liquid Shippers further argued, citing the ROE Policy Statement, that “the uncertainty surrounding the Commission’s oil pipeline ROE policy undermines the reliability of the reported ROEs for 2019.”[24] The pipelines, including LEPA (then known as the Association of Oil Pipe Lines (AOPL)), opposed the Liquid Shippers’ proposal by: (1) disputing that the reported ROEs were unreliable, (2) noting the Commission’s finding that statistical data trimming is sufficient to remove outlying equity cost changes, and (3) asserting that adopting Liquid Shippers’ proposal would “complicate the five-year review by introducing complex cost-of-service ratemaking issues.”[25]

The Commission rejected Liquid Shippers’ proposal. First, the Commission held that Liquid Shippers had failed to demonstrate that the pipelines’ self-reported ROEs are unreliable, and emphasized that those ROEs are based upon “established ratemaking techniques.”[26] The Commission rejected the premise that variation among page 700 ROEs renders them unreliable, and observed that “although the Commission typically sets the real ROE for oil pipelines at the median of the proxy group results, it may set the ROE above or below the median where the record demonstrates that the pipeline faces anomalously high or low risks.”[27] With respect to Liquid Shippers’ proposed standardized ROEs at that time, the Commission held that “Liquid Shippers [did] not demonstrate that this figure accurately measure[d] the investor-required cost of equity for all pipelines in the data set,” and stated that “[g]iven that oil pipelines have diverse business models and different risks levels, we simply cannot assume that any single ROE could reflect the investor-required return for all pipelines in the data set.”[28] Finally, the Commission concluded that “adopting Liquid Shippers’ proposal would undermine indexing’s purpose as a simplified and streamlined ratemaking regime,” noting that “[d]etermining a just and reasonable ROE, particularly on an industry-wide basis, would be a complex and fact-intensive inquiry” and the Commission’s previously-expressed concern that “addressing such complex cost-of-service issues would improperly complicate and prolong the five-year review process in violation of EPAct 1992’s mandate for simplified and streamlined ratemaking.”[29]

The Commission’s reasoning in the 2020 Final Rule was sound and, facing a proposal with the same fundamental flaws, is equally compelling now.[30] As in 2020, LEPA’s ROE Modification proposal purports to demonstrate that a “single ROE could reflect the investor-required return for all pipelines in the data set,”[31] a premise that the Commission previously rejected. In so doing, using the proposed ROE Modification sands down the Commission’s use of pipeline-specific risk assessment into a rote mathematical exercise, then imputes a single risk profile and associated ROE to an entire industry.[32] This inherent flaw is no different than that which the Commission rightly rejected in the 2020 Final Rule.

While the order acknowledges and attempts to distinguish this precedent, the distinctions are not compelling. The order concludes that this situation is different because “the reported data for 2019 and 2024 reflect different ROE policies,” while the Liquid Shippers’ prior proposal involved a single ROE policy.[33] That distinction has no relevance to the concerns articulated by the Commission in the 2020 Final Rule, which were inherent to the exercise of calculating a single, industry-wide ROE. The order then states that LEPA’s proposal to calculate an industry-wide ROE “coheres with EPAct 1992’s mandates for simplified and streamlined ratemaking,”[34] notwithstanding that Liquid Shippers’ similar proposal ran afoul of that same concern in the 2020 Final Rule.[35] At its core, the order does not actually distinguish the 2020 Final Rule, but instead concludes that the “benefits” of an “apples to apples” comparison between 2019 and 2024 ROE data warrant overlooking the shared flaws of LEPA and Liquid Shippers’ proposals.[36] I disagree that a single ROE could reflect the diverse risk profiles and associated investor-required return for all pipelines.

3. The Pipelines’ Own Reported ROEs Undermine the Premise that a Single Industry-Wide ROE Can or Should be Applied

Even if the order adequately distinguished Commission precedent that is squarely on point, it would still need to establish that LEPA’s proposed modification using a uniform 8.3% ROE reflects the risk profile and associated equity return for the roughly 150 pipelines to which it would apply.[37] The order does not. Notwithstanding LEPA’s effort to substantiate that its proposed 8.3% ROE is a reasonable industry-wide estimate, there is a more compelling data set that rebuts the premise of LEPA’s proposal: the pipelines’ own reported ROEs.

If it were reasonable to assume that the oil pipeline industry as a whole is largely homogenous and reflects companies of the same investment risks, then one would expect the pipelines themselves to report largely similar ROEs in their annual page 700 filings. Yet, the pipelines’ filed page 700 data show precisely the opposite, with wide-ranging ROEs that presumably reflect the pipelines’ own assessment that their risk profiles differ because their businesses, sources of revenue, and cost drivers vary greatly. The pipeline’s own reported ROEs thus contradict the notion that they face comparable investment risks such that it is reasonable to use the same 8.3% 2019 ROE for all of them. For instance, even trimming the data set to the middle 50%, the pipelines’ filed 2019 ROEs included 8.4% for Yellowstone Pipeline LLC and 16.2% for Tallgrass Pony Express Pipeline LLC. Similarly, the 2024 ROEs filed by pipelines in the middle 50%, which presumably incorporated the CAPM-based ROEs, included similar variation such as 8.39% for Valero Partners PAPS LLC and 16.2% for Caliber Bear Den Interconnect LLC. Moreover, illustrating the wide range of investment risks faced by various pipelines, the betas (representing each company’s volatility of performance relative to the overall stock market’s) in the Order No. 586 proxy group range from 0.780 for Magellan Pipeline to 1.041 for Enbridge Pipeline.[38] These betas do not represent values of a relatively homogenous group of pipelines that face the same risks and thereby justifies using a single ROE applied across roughly 150 pipelines.

Simply put, both things – that the pipelines’ self-reported but divergent ROEs are reasonable and reliable, and a single 8.3% ROE value reasonably reflects their uniform risk profile – cannot simultaneously be true. Through multiple five-year index proceedings over the last decade, the Commission has relied upon the accuracy of the pipelines’ own filed ROE data.[39] We and the pipelines cannot have it both ways. If we are to rely on the accuracy of the pipelines’ filed page 700 data as a foundation for the index itself, then we cannot simultaneously conclude that it is appropriate to use a uniform, industry-wide ROE in the index for this cycle.

I respect and understand the desire to fix the asymmetry in the data set. Accurate and transparent data are foundational to good ratemaking, and I take seriously the task of getting the index right. While the Commission does not need to demonstrate that a solution is perfect, adopting a single CAPM-based ROE that is methodologically flawed and rebutted by substantial evidence elsewhere in the record is not a viable solution to the asymmetry. The Commission is governed by its precedent and bound by the record before it, and I believe neither supports adoption of LEPA’s proposal in this case.

4. The ROE Modification Creates Inconsistent and Unreliable Results

While the ROE Modification purports to solve the asymmetry, it also creates other methodological problems that undermine the reliability of the index.

First, in attempting to address one asymmetry – that pipelines’ reported 2019 ROEs do not incorporate CAPM while their 2024 reported ROEs presumably do – the order creates other problematic asymmetries in the ROE data. Under LEPA’s proposal, the 2019 data now blend pipeline-specific ROEs (reflecting each pipeline’s assessment of its own risk profile) with a uniform 8.3% CAPM-derived ROE (premised on the idea that every pipeline faces identical level of investment risks). The order then compares the blended 2019 ROEs with the pipeline’s reported 2024 ROEs that presumably reflect each pipeline’s assessment of its own risk profile under both DCF and CAPM. This approach is not a methodologically-sound “apples to apples” assessment of comparable starting and end points, which introduces further methodological inconsistencies into the index analysis.

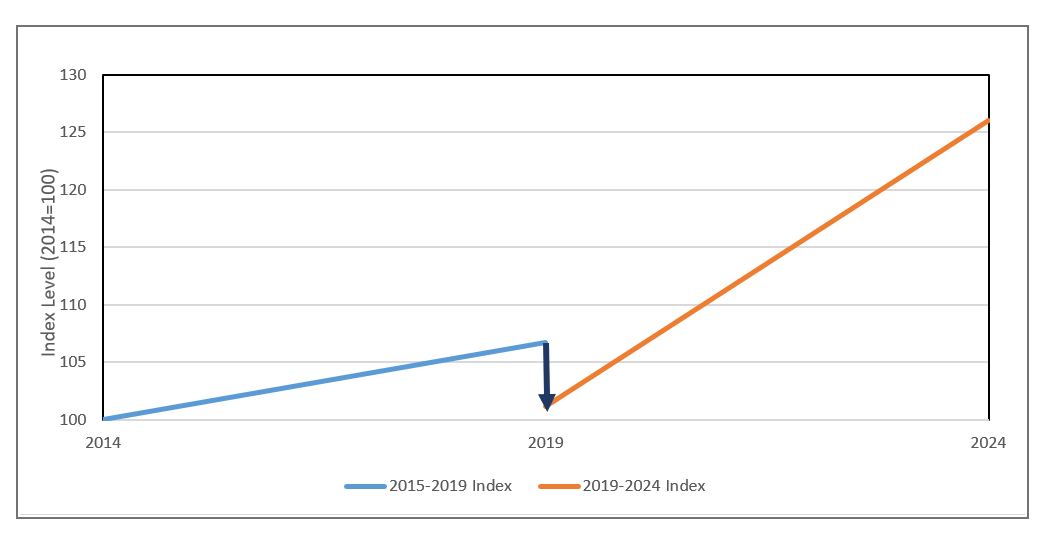

Furthermore, in attempting to create more of an “apples-to-apples” comparison for the 2019 and 2024 ROEs, the ROE Modification creates a “stitching problem” or a discontinuity between the current and prior index periods. Specifically, Figure 1 below illustrates that the 2014-2019 data used to derive the prior index included the higher DCF-only ROE for the year 2019. The ROE Modification applied to the 2019 data used for the 2019-2024 index comparison at issue here is predicated on the fiction that the 2019 ROE was significantly lower.[40] As a result of the ROE Modification, the pipelines’ calculated cost per barrel-mile at end of the first index period would be higher than that at beginning of the second index period, even though both purport to measure data for the same year (2019), creating an inconsistency and a “stitching problem” or an analytical discontinuity. Because the indices for every five years create a cumulative effect, with the indices building on the previous ones, the net effect of the discontinuity is an upward bias to the index. The combined impact of using LEPA’s proposed ROE Modification would cause the cost changes over the ten years between 2014-2024, and the associated rate increases authorized by the indices relying upon data from this time period, to be much higher than having a consistent approach for the whole period.

Figure 1: 2014 - 2019 and 2019 - 2024 Index Levels with ROE Modification Applied to the 2019 – 2024 Index

5. The Commission Can and Should Rely on the Pipelines’ Filed 2019 Data, as Any Methodologically Correct Solution Requires Pipeline-Specific Analysis

Having explained why the ROE Modification is flawed as a matter of policy, precedent, and record, I want to address what an appropriate remedy to the asymmetry would look like. This requires additional context about how the Commission ended up where we are.

As discussed above,[41] the Commission’s ROE Policy Change in May 2020 altered how each pipeline was required to determine its ROE and thus impacted how certain cost data are reported on page 700. Since the index is derived by measuring cost changes over a five-year period, in a perfect world, the starting and end points of that five-year period would be calculated using largely consistent approaches. The Commission recognized as much in the ROE Policy Statement, as it expressly “encourage[d] oil pipelines to file updated FERC Form No. 6, page 700 data for 2019 reflecting the revised ROE methodology established herein.”[42] This solution – specific adjustments to the pipelines’ reported ROEs, based on each pipeline’s assessment of its risk profile – was and is the methodologically-appropriate way to capture any effects of the ROE Policy Change. Had the pipelines updated their ROEs as the Commission encouraged,[43] then the asymmetry would have been solved and we would not be in our current predicament.

Unfortunately, almost all jurisdictional pipelines declined the Commission’s invitation, without explanation or justification, to update their ROE to reflect the ROE Policy Change. Only a minority of pipelines ever sought to revise their ROEs, and most of those waited roughly five years to do so, right before the commencement of the current index cycle.[44] And it is this combination of events – the ROE Policy Change, coupled with the pipelines’ subsequent decision not to timely revise their filed 2019 ROE data – that created the problem now before the Commission.[45]

So, given the record before us, the Commission must decide how to proceed. The order incorrectly presumes that the ROE Policy Change requires a change to the pipelines’ filed 2019 ROEs and applies the flawed ROE Modification to implement that change. Instead, the more defensible approach is that Commission should simply rely on the pipelines’ filed 2019 ROEs, which the pipelines represented under oath were accurate and declined to update when encouraged to do so. This conclusion would be consistent with the Commission’s broader reliance on page 700 data as a reliable foundation for the index, and would send an appropriate signal to the industry that the Commission expects them to maintain accurate and up-to-date information in their page 700s.[46]

III. The Order Errs by Deriving the Index Using the Middle 80 Data Set Rather than the Middle 50

As discussed below, the record and Commission precedent support adoption of the middle 50% data set, rather than the middle 80% data set reflected in the Final Rule.

A. Background

As the Commission has explained, the “purpose of the index is to permit a simplified recovery for normal cost changes, not to enable recovery for extraordinary cost increases or decreases.”[47] Data trimming helps the Commission achieve that purpose. Specifically, under the Kahn Methodology, after each pipeline’s cost change on a per barrel-mile basis is determined, the Commission trims the data set to remove statistical outliers and spurious data. While the Commission has adopted different data trimming approaches, its most common approach has been to trim to the middle 50% of reported data, which the Commission has found effectively removes pipelines with anomalous changes from the data set.[48]

In the NOPR, the Commission proposed to use the middle 80% of reported data. Noting that the Commission used the middle 80% in the most recent 2020 index review, the NOPR preliminarily concluded that “it is appropriate to consider more data in measuring industry-wide cost changes rather than less,” and that “‘normal’ cost changes are best defined using the inclusive data sample embodied in the middle 80%.”[49] The Commission affirms these findings in the Final Rule, while also concluding that the middle 80% “achieves a reasonable balance that incorporates a wide spectrum of industry experience while removing data that could distort the index calculation.”[50]

B. Commission Precedent and the Record Support Adoption of the Middle 50% Data set

Based on my assessment of the record, I conclude that the middle 50% data set better aligns with the logic and purpose of the indexing methodology, as well as relevant Commission precedent.

In each five-year index cycle, the Commission must first decide the appropriate data set to use, which it determines through assessment of the pipelines’ calculated per-barrel-mile cost changes. On this record, the middle 50% data set is the superior distillation of representative cost changes across the industry. First, that data set conforms with the index’s stated purpose of reflecting normal industry-wide cost changes through its identification of the data set’s central tendency. Furthermore, the middle 50% data set captures 82% of all reported barrel miles, demonstrating that it is broadly representative of the cost of transporting oil and refined products across jurisdictional pipeline systems.[51]

Furthermore, the weight of Commission precedent supports adoption of the middle 50%, as the Commission’s reasoning in those proceedings aligns with the record evidence here. The Commission has repeatedly recognized the benefits of trimming to the middle 50% compared to other approaches, including the middle 80% alternative.[52] The Commission has also emphasized that “statistically trimming the data set to the middle 50 percent already removes anomalous cost/barrel-miles changes,”[53] which reduces the need for manual trimming or data adjustments. This approach is thus better aligned with Congress’ statutory directive to develop a streamlined and simplified ratemaking design.

I also disagree with the order’s conclusion that the middle 80% represents a superior data set for capturing normal industry cost changes. While this data set incorporates a substantial number of additional pipelines, it adds only a relatively marginal increase in barrel miles, which increases the risk that anomalous or non-representative data are introduced into the central tendency analysis. Were the data distributed in a statistically normal manner, the difference between data trimming to the middle 50% would not differ materially from trimming to the middle 80%. However, because the data set is skewed to the right with more outliers with costs higher than the mean or median, leaving a greater number of outliers upwardly biases the result. Because the index is intended to reflect typical pipeline costs increases, more substantial trimming is particularly important where the distribution is shifted rightward or leftward. Adding more data does not necessarily improve the data set, and reliance on the middle 50% avoids these unnecessary risks.

I am similarly not persuaded by the order’s reliance on the 2020 Final Rule as support for deviating from the Commission’s reliance on the middle 50% data set in the 2010 and 2015 index cycles. The most recent 2020 index cycle was an unusually unstable exception to the Commission’s use of the middle 50%,[54] so I assign the Commission’s adoption of the middle 80% in that proceeding limited precedential weight, particularly given that the Commission’s adoption of the middle 50% was repeatedly affirmed on appeal.[55]

IV. The Record Supports an Index of (PPI-FG) – 1.68%

Given my disagreement with two critical determinations in the Final Rule and based on my review of the record, I support adoption of a final index level of (PPI-FG) – 1.68%.[56] As discussed above, I believe this value is consistent with Commission precedent and supported by the full record before us. I take this opportunity to address two additional points regarding the index: (1) the implications of a “PPI-FG minus” index value, and (2) the alternative ratemaking options available to pipelines.

A. The Appropriate Approach Yields an Index Lower than PPI-FG Due to Inflationary Period between 2019 through 2024

All but one of the index proposals in the record – even that from LEPA – result in an index lower than PPI-FG. This reflects the fact that pipelines’ reported costs were less than inflation over the relevant preceding five-year period. Given the well-documented, economy-wide inflation experienced between 2019 and 2024, the resulting negative index is simply an artifact of the approach used in setting the index relative to the inflation rate in the preceding five years. For instance, the Commission’s adopted index levels for 2021-2026 authorized pipelines to increase their ceiling levels by roughly 30% over just that five year period,[57] with the overwhelming majority of that increase driven by the PPI-FG index itself, rather than the Commission’s annual +0.78% index adjustment. Thus, the level below the PPI-FG properly reflects the oil pipelines’ cost changes relative to the past five years’ inflation rate and therefore carried forward using future inflation rates. Should pipelines’ reported costs exceed inflation in this upcoming five-year period, then that differential will be captured in the next index cycle, as contemplated through the simplified index design.

B. Pipelines Have Multiple Ratemaking Options, Including for the Development of System Expansions

Finally, the indexing methodology is designed to approximate a simplified cost-of-service framework,[58] through which the Commission considers the interests of both pipelines and shippers in setting rates. I conclude that the alternative index value of (PPI-FG) – 1.68% that relies on the middle 50% dataset and pipelines’ self-reported ROE values is consistent with Commission precedent, supported by the record before us, and reasonably balances those competing interests. To the extent that an individual pipeline experiences abnormally high expenses that exceed recovery through the index framework, then it may pursue a cost-based rate. Furthermore, major pipeline expansions can be developed through negotiated and settlement rates that deviate from indexed rates, consistent with longstanding Commission precedent.[59]

V. Conclusion

Action on the five-year oil index is among the most consequential decisions any Commissioner issues during his or her tenure. Today’s order will likely shift billions of dollars between pipelines and shippers over the next five years, and given the cumulative nature of the index, will have repercussions long past this cycle. Furthermore, higher transportation costs via indexed rates will have a real-world financial impact, including to consumers that use oil or other petroleum-derived products. The result reached in today’s order is not adequately supported by the record or Commission precedent.

While I disagree with today’s order, I respect my colleagues’ assessment of the record and the different conclusion that they reached; our disagreement followed robust internal discussions, and resolution of this proceeding will presumably rest with the appellate courts. In the meantime, I look forward to collaborating with my colleagues through other proceedings to continue to faithfully implement our responsibility to ensure cost-effective and non-discriminatory transportation service under the ICA.

For these reasons, I respectfully dissent.

[1] Five-Year Rev. of the Oil Pipeline Index, [add cite] (2026) (Final Rule).

[2] Pub. L. No. 102-486, 1801(a), 106 Stat. 2776, 3010 (Oct. 24, 1992), codified at 42 U.S.C. 7172 note.

[3] Revisions to Oil Pipeline Regulations Pursuant to Energy Pol’y Act of 1992, Order No. 561, FERC Stats. & Regs. ¶ 30,985, at 30,947 (1993) (cross-referenced at 65 FERC ¶ 61,109), order on reh’g, Order No. 561-A, FERC Stats. & Regs. ¶ 31,000 (1994) (cross-referenced at 68 FERC ¶ 61,138), aff’d sub nom. Ass’n of Oil Pipe Lines v. FERC, 83 F.3d 1424 (D.C. Cir. 1996).

[4] E.g., 18 C.F.R. § 342.4 (specifying cost-of-service rates, market-based rates, and settlement rates as alternative rate methodologies to indexing); see also Order No. 561-A, FERC Stats. & Regs. ¶ 31,000 at 31,097 (“Extraordinary costs can be recovered through either of the alternate rate change means—cost of service or settlement rates—as provided in [Order No. 561].”); Saddlehorn Pipeline Co., LLC, 169 FERC ¶ 61,118 (2019) (approving rates, terms, and conditions established through an open season for a system expansion).

[5] Since 2015, the Commission has relied upon data submitted by pipelines via page 700 of Form 6 to calculate the industry-wide cost changes used to establish the index. Five-Year Rev. of Oil Pipeline Index, 153 FERC ¶ 61,312, at PP 12-18 (2015) (2015 Final Rule), aff’d sub nom. Ass’n of Oil Pipe Lines v. FERC, 876 F.3d 336 (D.C. Cir. 2017) (AOPL III).

[6] If pipelines’ observed cost changes are lower than inflation as measured by PPI-FG, then the index will be a negative number. If pipelines’ observed cost changes are higher than inflation as measured by PPI-FG, then the index will be a positive number.

[7] These multipliers are posted each year by the Commission. FERC, Oil Pipeline Index Indexing Methodology – Indices to be Used, https://www.ferc.gov/general-information-1/oil-pipeline-index. The posted multiplier can vary significantly, largely driven by whether inflation (as measured via PPI-FG) is higher or lower. For example, the multiplier for July 1, 2021 – June 30, 2022 (derived during the first year of the COVID pandemic, when inflation was very low) was 0.994188, i.e., a reduction in the pipelines’ ceiling rates. By comparison, the multiplier for July 1, 2022 – June 20, 2023 (i.e., derived as the economy emerged from the COVID pandemic, when inflation was high) was 1.097007, i.e., a nearly 10% increase in the pipelines’ ceiling rates.

[8] So, for example, assume the Commission adopted an index of +1%. If the PPI-FG inflation measure for year one of the five-year cycle was 2%, then the annual multiplier would be 1.03, i.e., a 3% increase in pipelines’ ceiling rates. If the PPI-FG measure for year two was 3%, then the multiplier for that year would be 1.04%, and the net increase of pipelines’ ceiling rates across both years would be 7.12% (i.e., 1.03 * 1.04).

[9] Before turning to the merits of these issues, I have one point of clarification. My assessment of this proceeding is informed and bound by the Commission’s adoption of the Kahn Methodology, applied to pipelines’ filed page 700 data, as its chosen means of satisfying Congress’ mandate for a “simplified and generally applicable” ratemaking methodology. I am under no illusion that this methodology or data set are perfect, and both contain analytical or evidentiary shortcomings. I am open to future refinements to the methodology and data set to ensure that subsequent index cycles are as analytically sound as possible.

[10] 2015 Final Rule, 153 FERC ¶ 61,312 at P 14 (noting that the Commission previously “used net carrier property as a proxy for capital costs and income taxes”).

[11] Ass’n of Bus. Advocating Tariff Equity v. Midcontinent Indep. Sys. Operator, Inc., Opinion No. 569, 169 FERC ¶ 61,129 (2019).

[12] Inquiry Regarding the Comm’n’s Pol’y of Determining Return on Equity, 171 FERC ¶ 61,155 (2020) (ROE Policy Statement).

[13] Pursuant to the schedule provided in the section 357.2(b)(2) of the Commission’s regulations, oil pipelines submitted their 2019 page 700 data in April 2020, one month prior to the Commission’s announcement of the ROE Policy Change.

[14] ROE Policy Statement, 171 FERC ¶ 61,155 at P 92.

[15] Inquiry Re: the Commission’s Policy for Determining Return on Equity; Five-Year Review of the Oil Pipeline Index, Docket Nos. PL19-4-000 and RM20-14-000 (July 7, 2020).

[16] Five-Year Rev. of the Oil Pipeline Index, 193 FERC ¶ 61,145, at P 6 (2025) (NOPR).

[17] Id. P 13.

[18] Final Rule, [add cite] at P 12.

[19] As discussed below in section II.C.5, use of the pipelines’ filed 2019 data is consistent with the Commission’s broader reliance on the accuracy of page 700 data and is an appropriate resolution on this record, given that the pipelines’ election not to update their filed ROEs following the ROE Policy Change.

[20] ROE Policy Statement, 171 FERC ¶ 61,155 at P 6 (emphasis added).

[21] NOPR, 193 FERC ¶ 61,145 at P 13, n.31; Final Rule, [cite] at PP 28, 31.

[22] Five-Year Rev. of Oil Pipeline Index, 173 FERC ¶ 61,245, at P 41 (2020) (2020 Final Rule), order on reh’g, 178 FERC ¶ 61,023 (2022) (2022 Rehearing Order), reh’g denied, 179 FERC ¶ 61,100 (2022), vacated sub nom. Liquid Energy Pipeline Ass’n v. FERC, 109 F.4th 543 (D.C. Cir. 2024), order following vacatur, 188 FERC ¶ 61,173 (2024), order on reh’g, 193 FERC ¶ 61,137 (2025).

[23] Id.

[24] Id. P 42.

[25] Id. P 44.

[26] Id. P 46.

[27] Id. P 47.

[28] Id. P 49 (emphasis added).

[29] Id. P 50 (emphasis added).

[30] Ironically, LEPA (then known as AOPL) objected to the Commission’s 2015 decision to use page 700 data in part because of its concern about the volatility of pipeline ROEs, yet now argues it is reasonable to apply a single ROE value to roughly 150 pipelines, representing approximately 75% of the relevant data set. 2015 Index Final Rule, 153 FERC ¶ 61,312 at P 10.

[31] 2020 Final Rule, 173 FERC ¶ 61,245 at P 49.

[32] As discussed below, the record also contains substantial and compelling evidence that this imputed ROE has no correlation to the pipelines’ assessment of their own risk profiles and resulting ROEs.

[33] Final Rule, [add cite] at P 28.

[34] Id. P 31.

[35] 2020 Final Rule, 173 FERC ¶ 61,245 at P 50. Compounding matters, the order then notes that shippers “have not proposed a superior alternative adjustment” to LEPA’s proposal, notwithstanding (1) they had no obligation to do so, (2) the NOPR proposed not to make an adjustment for reasons consistent with the Commission’s findings in the 2020 Final Rule, and (3) the Commission soundly rejected their last attempt to propose a uniform ROE in 2020. Final Rule, [add cite] at P 31.

[36] Final Rule, [add cite] at P 27 (“Although we recognize that any changes to the reported page 700 introduce a degree of additional complexity, we conclude that the benefits of more accurately measuring actual industry cost changes during the five-year review period by using consistent ratemaking policies support adjusting the reported data notwithstanding these concerns.” (emphasis added)); id. P 31 (“To the extent that LEPA’s proposed CAPM return does not precisely measure the cost of equity for all pipelines in the data set, this imprecision is justified by the need to resolve the data incongruities resulting from the ROE Policy Change.” (emphasis added)).

[37] 2020 Final Rule, 173 FERC ¶ 61,245 at P 49 (rejecting Liquid Shippers’ uniform ROE proposal because they “do not demonstrate that this figure accurately measures the investor-required cost of equity for all pipelines in the data set” (emphasis added)).

[38] LEPA Dec. 29, 2025 Initial Brief, Ex. No. MJW-L2 – ROE Results at CAPM Results tab.

[39] See, e.g., 2020 Final Index, 173 FERC ¶ 61,245 at P 46 (recognizing that pipelines submit their page 700 data under oath and rejecting arguments that the submitted data are unreliable); 2015 Final Index, 153 FERC ¶ 61,312 at PP 12-18 (explaining benefits of page 700 data as a “superior data source for use in the Kahn Methodology”). The D.C. Circuit Court of Appeals has also affirmed the Commission’s decision to use these filed data for the index. AOPL III, 876 F.3d at 344-46 (rejecting challenge to Commission’s adoption of page 700 data in the 2015 Final Rule).

[40] Figure 1 is derived from the Brattle Group Reply Report appended to the Joint Commenters’ Reply Brief. Joint Commenters Jan. 20, 2026 Reply Br., Brattle Group Reply Report at PP 86-87, Fig. 6.

[41] Supra at section II.A.

[42] ROE Policy Statement, 171 FERC ¶ 61,155 at P 92.

[43] As the order observes, subsequent to the ROE Policy Change, the Commission issued Opinion No. 586, which “further refined its ROE methodology….” Final Rule, [add cite] at n.117. While the order characterizes these refinements as “not reflect[ing] the same ROE policy” as the ROE Policy Statement, these changes were incremental rather than substantial. Id. In any event, pipelines also did not propose to revise their 2019 ROE data following the issuance of Opinion No. 586.

[44] In the NOPR, the Commission preliminarily addressed updated 2019 data submitted by 61 pipelines beginning in April 2025, five years after these cost data were originally due, by proposing to exclude those data from its calculation of the index. NOPR, 193 FERC ¶ 61,145 at PP 15-16. The Final Rule largely sustains this proposed finding by rejecting the non-ROE related “corrections” and excluding those data from the final index value adopted in the order. Final Rule, [cite] at PP 40-41. I agree with that decision for the reasons stated in the order, and the Commission should expect pipelines to submit timely revisions to page 700 data if the information on file is incorrect. With respect to the pipelines’ ROE-related adjustments, the Final Rule finds that the ROE Modification “sufficiently and more effectively” addresses the ROE Policy Change, as “using the ROEs in the resubmitted filings and making the [ROE Modification] for the remaining pipelines could lead to inconsistent treatment of the ROEs across the whole data set.” Id. P 42. For the reasons articulated in the NOPR, I would also exclude the pipelines’ late-filed attempt to update their 2019 ROE-related data.

[45] Unfortunately, I think the order misdiagnoses the issue before us as simply the asymmetry resulting from the ROE Policy Change, while failing to account for the contributing role of the pipelines’ own inaction. This assessment then leads the order to assume responsibility for fixing a problem that the Commission did not solely create, while absolving the pipelines of their role and adopting their preferred but fundamentally flawed solution instead.

[46] This approach also would be consistent with the Commission’s reasoning for declining to apply the ROE Modification to pipelines that reported an identical ROE across the full 2019-2024 data set. Final Rule, [add citation] at P 25 (electing not to apply the ROE Modification to pipelines that reported the same ROE because “the ROE Policy Change does not appear to have affected how the pipeline reported its ROE on page 700, and it is not clear that each of these pipeline’s 2019 data reflect different Opinion No. 154-B policies than their 2024 data.”).

[47] Five-Year Rev. of Oil Pipeline Pricing Index, 133 FERC ¶ 61,228, at P 61 (2010) (2010 Index Review), reh’g denied, 135 FERC ¶ 61,172 (2011).

[48] Infra P 39.

[49] NOPR, 193 FERC ¶ 61,145 at PP 9-10.

[50] Final Rule, [add cite] at PP 49-52.

[51] This sample size captures an even larger percentage of barrel miles than prior instances in which the Commission relied on the middle 50 data set. See, e.g., 2010 Final Rule, 133 FERC ¶ 61,228 at P 63 (finding that the “middle 50 percent of pipelines represents 76 percent of total barrel-miles in 2004 subject to the index, and thus for this index calculation, the Commission finds it unnecessary to include the middle 80 percent to obtain a representative sample of the data”); 2015 Final Rule, 153 FERC ¶ 61,312 at n.85 (noting that “the statistically trimmed data set includes more than 50 percent of industry barrel-miles”).

[52] See, e.g., 2015 Final Rule, 153 FERC ¶ 61,312 at PP 42-44; 2010 Final Rule, 133 FERC ¶ 61,228 at P 61 (“The middle 50 percent more appropriately adjusts the index levels for ‘normal’ cost changes as opposed to the middle 80 percent, which, by definition, includes pipelines relatively far removed from the median.”); id. (“Even when accurate data is reported, pipelines in the middle 80, as opposed to the middle 50, are more likely to have cost changes resulting from factors particular to that pipeline, such as a rate base expansion plant retirement, or localized changes in supply and demand. Using the middle 50 ensures that pipelines with relatively large cost increases or decreases do not distort the index.”).

[53] 2015 Final Rule, 153 FERC ¶ 61,312 at P 23.

[54] While it is true that the ultimate outcome of the 2020 index review cycle was the adoption of the middle 80% data set, the actual story is far more complicated. In the 2020 Final Rule, the Commission adopted the middle 80% data set on a split Commission vote. 2020 Final Rule, 173 FERC ¶ 61,245. Via a subsequent bipartisan vote on rehearing, the Commission reverted to the middle 50% data set, consistent with longstanding precedent. 2022 Rehearing Order, 178 FERC ¶ 61,023. That order was vacated on appeal on procedural grounds, and the Commission subsequently elected, for prudential reasons, to leave the 2020 Final Rule intact. Supplemental Review of the Oil Pipeline Index Level, 193 FERC ¶ 61,136, at P 20 (2025) (Supplemental Order). Shippers’ appeals of the 2020 Final Rule and the Supplemental Order are pending before the D.C. Circuit. As a result, no court has actually assessed, let alone affirmed, whether the Commission’s adoption of the middle 80% in the 2020 cycle was appropriate.

[55] E.g., Flying J Inc. v. FERC, 363 F.3d 495 (D.C. Cir. 2004) (affirming the Commission’s decision, following remand, to adopt a middle 50 data set); AOPL III, 876 F.3d at 342-44.

[56] I derived this index level by modifying the Final Order’s adopted data set by (1) removing the ROE Modification and instead relying on the pipelines’ filed ROE data, and (2) using the middle 50% instead of the middle 80% data set. Otherwise, my analysis relies upon the data set approved by the Final Rule, including the accuracy of limited data corrections and assumptions incorporated into the data set. Specifically, I eliminated the addition of the 8.3% ROE Modification the New_NormalizedData tab and the Refile Adjust tab, in both cases leaving the originally filed ROEs.

[57] FERC, Oil Pipeline Index Indexing Methodology – Indices to be Used, https://www.ferc.gov/general-information-1/oil-pipeline-index. I derived this value simply by multiplying each of the authorized index values from July 1, 2021 through June 30, 2026. That inflation was particularly pronounced in the two years from July 1, 2022 through June 30, 2024, in which the annual index increases were 9.7% and 14.3%, respectively.

[58] See, e.g., 2015 Index Review, 153 FERC ¶ 61,312 at P 13 (finding that “the index is meant to reflect changes to recoverable pipeline costs, and, thus, the calculation of the index should use data that is consistent with the Commission’s cost-of-service methodology”).

[59]See, e.g., Saddlehorn Pipeline Co., LLC, 169 FERC ¶ 61,118 (2019); see also 18 C.F.R. § 342.2 (providing that a carrier must justify an initial rate for new service by either submitting “cost, revenue, and throughput data supporting such rate” or “[f]iling a sworn affidavit that the rate is agreed to by at least one non-affiliated person who intends to use the service in question”).